In the business of risk transfer, brokers are an essential link in a chain that manages the flow of risk and capital. The most significant stakeholders to any broker are the client and the insurer. IoT is changing the way brokers monetise these relationships:

- Placement of risk moves from speculative to highly targeted.

- Client services move from low-frequency transactions to high-frequency consultation.

These two changes alter the broker business model, emphasising relationships by creating value from a broker’s understanding of each stakeholders business.

With new features in Quest Marine, brokers will be able to realise the value of IoT and differentiate themselves in a crowded marketplace.

What’s IoT doing in the market today?

The internet of things (IoT) draws data on assets of interest from a wide range of sources. When curated properly, it allows you to build a more detailed profile of vessels, fleets, and accounts.

Insurers are leveraging these profiles to improve the way they understand and price risk. As more insurers move to incorporate big data analytics in risk assessment, brokers will face:

- A pressure to match the digital underwriter’s understanding of risk

- An opportunity to diversify and generate greater revenue opportunities

Brokers can acquire accounts insurers want

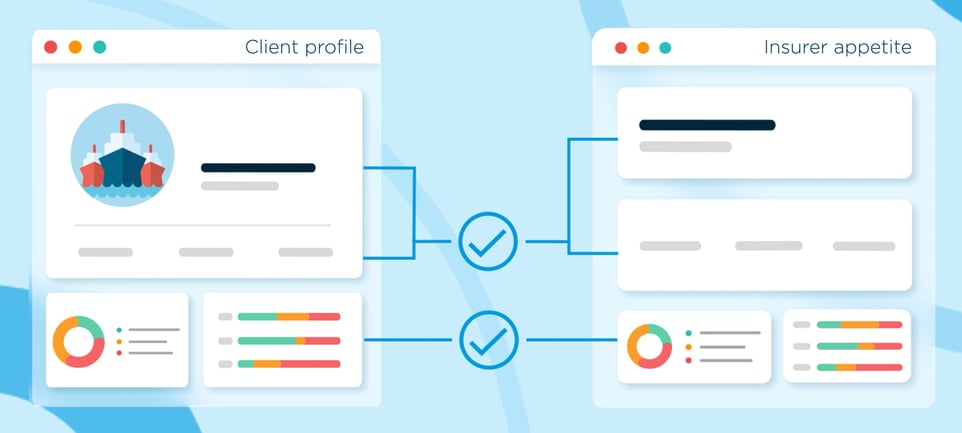

Access to global risk profiles means brokers can search for any account with an IMO. By using the insurer’s appetite as search parameters, every result will yield accounts that have a high chance of placement. Making this process digital means brokers can:

- Reduce the time taken to find key accounts

- Understand the drivers of value for each account before approach

- Maximise investment in client acquisition

Fig 1: Using an insurers appetite as search parameters, profiles with the highest chance of placement can be identified

Ready for negotiation

When a broker finds an account, they need to pitch it. Making this process digital ensures reports reflect key account information and are ready to share with those working remotely. Selecting key insights lets brokers:

- Prove the value of an account by emphasising information that supports negotiations

- Remove barriers for insurers that have not yet deployed platforms like Quest Marine

Ad hoc reports are currently used in traditional broker models. Augmenting a process brokers already familiar with reduces friction to change as the key principles remains the same.

Relationships are the backbone of a broker’s business. For particularly lucrative accounts, brokers can align with insurers on both account targeting and approach. This gives a broker confidence that they’re backed in principle, increasing conversion potential whilst catering to mutual interests. It also differentiates the broker within the insurer’s network, adding value to the relationship.

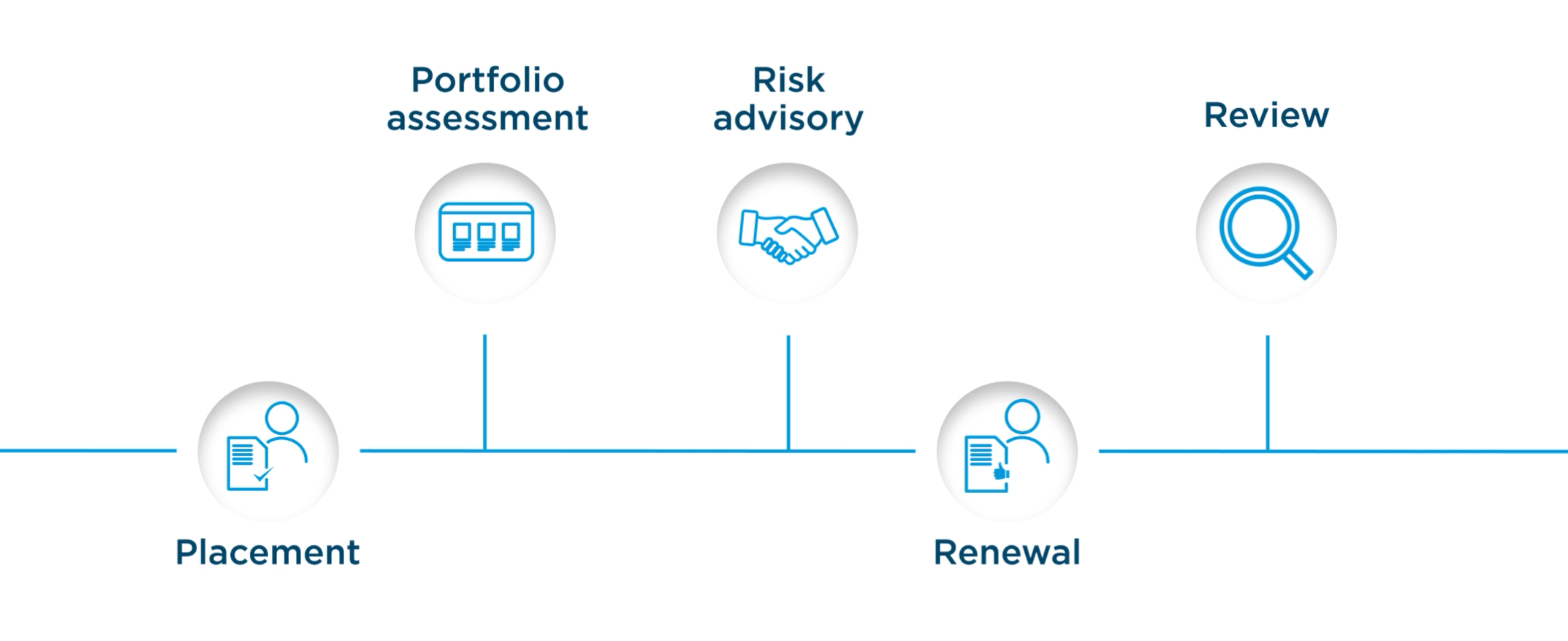

More value for clients

To date, Brokers are primarily deal makers, matching clients with the most appropriate cover. While risk advisory services are offered, there’s no doubt that the bulk of broker income comes from the placement of risk. This means a client will only need a broker in set circumstances, limiting the total number of touch points that can be monetised. It’s why relationships are so important, as these limited touch points have great weight on customer lifetime value.

Fig 2: Typical client-broker touch points.

Fig 2: Typical client-broker touch points.

Increasing total client touch points will provide more revenue opportunities. To increase total touch points, brokers will need to deliver more value. Access to the same vessel, fleet, and organisation profiles underwriters currently use will allow brokers to better understand how their clients are perceived. Translating this understanding to risk advisory services will help clients direct investment to areas of need, improving overall risk profile.

Pulling this insight into a branded report means that insight can distributed amongst clients without friction.

Fig 3: Adding value to risk advisory services increases total broker-client touch points.

The bottom line

Better client risk profiles mean lower premiums for clients, whilst the additional revenue unlocked through advisory services will yield greater returns per client long-term. When you combine the benefits of a higher placement rate, stronger relationship with insurers and increased conversion potential of new prospects, it’s clear digitalisation provides a greater potential for monetisation vs a traditional broking model.

For more on how applications like Quest Marine can help your business, get in touch.