The ‘digital revolution’ is upon us. What does this mean? What will the market look like when it is ‘digital’? How quickly will we get there?

Leading consultancies predict that, within the next five years, every insurer will need to transition into a ‘digital insurer’. This transformation can deliver a strong competitive advantage and offers potential operational cost reductions of c.30%. Gartner defines digitalisation as the process of moving to a digital business, using technologies to change business models for revenue and value-producing opportunities.

When applied to insurance, digitalisation fosters more than a change in infrastructure. It’s the catalyst for changing underlying operations, giving far greater reliance on advanced technology, data, and AI. The benefits come from a combination of the adoption of new technologies and a change in business process to account for new ways of working. Most roles will require digital upskilling and a sustained investment in people will be required to ensure they have the skills to operate in this new environment.

Retrospective understanding and technological change

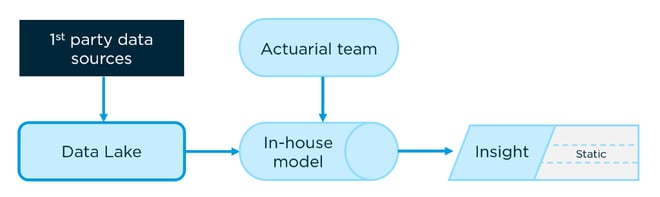

The application of big data and advanced analytics leads to a revised understanding of the risks that a customer might want to insure against. Information regarding historical events and losses is used to make judgements around future risk. Specifically, past events are quantified and extrapolated into a potential likelihood of occurrence in near real-time. To do this, data is currently drawn from in house assets, modelled by actuaries and translated to insight for underwriters. The core principles of insurance post digitalisation won’t change. What will change, is the way actuaries and underwriters go about daily activities.

Fig 1: Traditional process

Fig 1: Traditional process

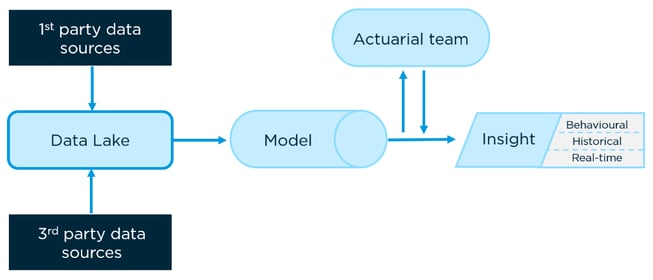

In the most basic terms, the overall volume of data available today has increased massively, and in the future the majority of data will have been externally curated. This is good, as it means Insurers and Brokers can draw from more information about the Insured. However talented, a team of Actuaries alone can’t interpret such a vast volume of data fast enough to deliver insight in a timeframe that’s useful for an Underwriter to maintain an advantage in the market. Therefore, automated techniques are applied to the data to draw insight. Actuaries can validate results and draw further understanding. They may use new capabilities to build new products and services for that insurer. Meanwhile, the advanced insight available to Underwriters from this process lets them form better and faster business decisions.

Fig 2: Modern process

Fig 2: Modern process

Whilst this method realises the retrospective aspect of the existing insurance model to the greatest extent, automation speeds up data collection. This means real-time insight can be applied, allowing insurers to see how the market is changing and how the Insured are behaving. Further adaptation to products and services can occur as a result.

This emphasises the move of Insurers and Brokers from ‘skill-based’ organisations to ‘knowledge-based’ organisations. Data assets provide the foundation for such knowledge, a single source of truth. Their scale and integrity are vital in determining the level of intelligence available to the organisation. Deciding what curated data forms part of your organisations’ data lake will define capabilities moving forward. The value of transformation is significant, with a fully digital insurer estimated to enjoy an operating expense ratio of 30% less than current ‘analogue’ insurers. The move from skill-based operators to knowledge-based operators will also change the nature of the market from one of risk transfer to one of risk mitigation.

You’ll notice that outside of the real-time nature of data collation, everything is related to retrospective analysis. This doesn’t account for a view of the future. The prospective nature of insurance, which is where the foresight and application of understanding come into play, needs human judgement. A balance is therefore always required between comprehensive retrospective analysis and prospective awareness. If the past equalled the future in totality, then our job would be done. If we needed proof that this wasn’t the case, the year 2020 delivered.

Prospective application

Improved intelligence provides a point of differentiation. Organisations will utilise such advantages to drive change and become more profitable. This touches every role within the organisation and employees will need to upskill to fully capitalise on the new capabilities available to them.

Models turn the product of algorithms into a measure of risk. We’ve discussed that the role of the Actuary will change to facilitate efficiency, validate outcomes, and facilitate development. The circumstances will mean that we will see more Actuaries adopt the core principles of Data Science to better serve such needs. Reinsurance will see Actuaries expand on models that draw data from industry standard data lakes in-line with bespoke requirements. In the future, all Actuaries will be Data Scientists, however not all Data Scientists will be Actuaries.

Underwriters are trusted to keep abreast of the industry and develop a view of the future i.e. a view on South-South trade, lower oil prices, Brexit, etc. However, they’ve typically been swamped with data analysis activities and reporting. With digitalisation making that process more efficient they’ll be able to assimilate and apply the full extent of their prospective activities. It’ll lead to what BCG refer to as the Bionic Underwriter, a hybrid of the art of underwriting with the Science of Data. The Bionic Underwriter will leverage technology to differentiate through operational efficiencies, market understanding and improved services.

We’ll see the ‘Bionic Underwriter’ become wholly dependent on such capabilities to compete effectively. We’ve seen a similar level of dependence on focussed technologies change the industry before. In the 1990s, when Direct Line insurance was structured entirely around the telephone without a fall-back operating model. If it wasn’t for the internet in the 2000s, the aggregators would fail. Without black boxes in vehicles, Progressive’s Slingshot business would fail. Without artificial intelligence (AI), Lemonade’s business model is inoperable. If a characteristic is seen as a competitive advantage, the business model must be dependent on it.

A dependency on advanced insight will lead Bionic Underwriters to restructure placement to better suit the level of intelligence available. At scale, a new placement model will rely on data-led insight and automation to focus on personalised policy structures, highly complex risk, product development and client/broker relationships.

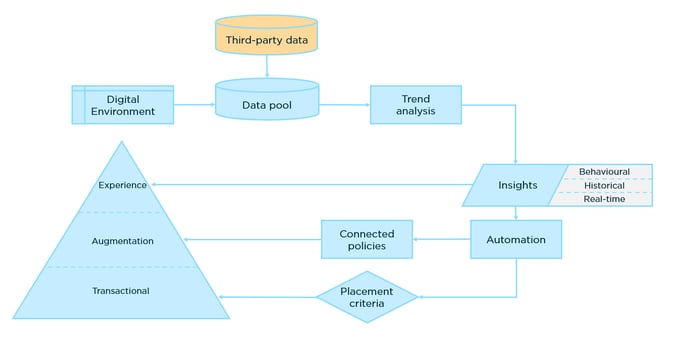

Fig3: New insurance placement model

Fig3: New insurance placement model

Automation optimises distribution, allowing for high, volume transactional business to be processed in-line with pre-defined criteria. This lets more Underwriters focus on applying their experience to higher value sales. Such enablement will help foster relationships and secure more attractive business. The adoption of new data sources ensures an in-depth understanding of customer needs and how that applies to the performance of the portfolio. Terms can be personalised relating to situation and time on cover, allowing the policy to match the exact needs of individual accounts. Augmentation through connected policies that leverage live monitoring of vessels, or the need for a completely bespoke set of requirements, become more economical to create and distribute. These examples express the value of data-led insight through its application, by an Underwriter, in context of the market. The influence of an Underwriters perception of market trends and matching insight to both market and portfolio conditions requires situational awareness, which is distinctly human.

Underwriters aren’t the only ones that will alter their business model to prospect in light of improved retrospective understanding. Brokers will benefit substantially from intelligence platforms, allowing them to diversify from annual transactions to long-term business models that add value. Having the same level of understanding as all other stakeholders in the market allows a Broker to better evaluate the suitability of a clients business. This means they can more accurately match risk to capital, sell services that improve a clients risk profile, consult on proactive risk management, negotiate terms that improve based on changes in performance (connected policies).

The ability for a Broker to review their client’s risk profile, benchmark against their peers, understand what markets are looking for and develop and deliver services whilst placing that risk, will lead to a significant escalation in Broker activity.

A great example of this is by looking at the way recruiters use LinkedIn. LinkedIn is a platform where companies manage their profile and advertise roles. Equally, employees manage their profiles and search for roles. You’d think LinkedIn would have made recruiters redundant, but it is in fact, their best tool, giving them access to a level of understanding they didn’t have before.

We’ve already adapted

Our everyday lives are the best demonstration of how these competencies will change the way organisations operate:

- The main method of navigating the internet is a search engine; using data and algorithms to make the volume of results manageable for us.

- Navigation through the sheer volume of items sold through Amazon is made simple with data-led recommendations, associated items, prior purchases, popularity, and reviews.

- When trying to get from point A to point B, we use Google Maps to process multiple routes, taking into consideration historic and predicted traffic patterns along with each person’s location in real-time. Would you rather look at a map book to plan a route?

We’ve accepted the quality of life benefits that data, algorithms and complex models provide. It is not possible for us to store, process and serve up an understanding of such vast amounts of data in an acceptable time. We now leverage them to guide most of our daily digital decisions. Our habits, and lives, have already changed around the efficiency they provide. Seamless human-digital interaction is no longer revolutionary, but a necessity. The move to a more bionic way of working is therefore well within reach.

Given the examples provided, specialty insurance is still considered to be at its inception regarding seamless human-digital interaction. The processes involved in creating such capabilities in-house are expensive, time-consuming and will be subsequently limited by the fact that you will always be a competitor over a supplier. InsurTechs like Concirrus accelerate digital transformation to provide a new view of risk through access to a comprehensive and curated data-lake, as well as data science expertise. This is applied at all levels, organisation-wide digital transformation projects, analytics platforms such as Quest, or project-specific consultancy with dedicated specialists. Get in touch to find out how we can work with your business.